Q1 2026 Market Volatility: Protect Your Retirement Portfolio Now

Navigating Q1 2026 Market Volatility: Practical Solutions for Protecting Your Retirement Portfolio

As we stand on the precipice of Q1 2026, the global economic landscape presents a complex tapestry of opportunities and challenges. For those in or nearing retirement, the specter of market volatility can be particularly daunting, threatening to erode years of diligent saving and meticulous planning. The question on many minds is: how do I effectively protect retirement portfolio amidst these turbulent times? This comprehensive guide delves into the anticipated market dynamics of early 2026 and provides actionable, time-sensitive strategies to safeguard your financial future.

The lessons learned from past economic downturns, coupled with forward-looking economic indicators, suggest that Q1 2026 could bring a period of renewed market flux. Geopolitical tensions, evolving monetary policies, technological disruptions, and shifting consumer behaviors are all contributing factors to this anticipated volatility. For retirees, whose time horizon for recovery is often shorter, proactive measures are not just advisable; they are imperative. Our goal here is to equip you with the knowledge and tools to not only withstand potential shocks but to also position your retirement portfolio for resilience and sustained growth.

Understanding the nuances of market movements and implementing robust protective strategies are key to ensuring that your hard-earned savings continue to work for you. From strategic asset allocation to exploring alternative investments and re-evaluating risk tolerance, every aspect of your financial plan deserves a thorough review. Let’s embark on this journey to fortify your retirement nest egg against the uncertainties of Q1 2026 and beyond.

Understanding the Q1 2026 Market Outlook

To effectively protect retirement portfolio, the first step is to gain a clear understanding of the potential forces at play in Q1 2026. Economic forecasts suggest a mixed bag of indicators. Inflation, while showing signs of cooling in some sectors, may remain a persistent concern, impacting purchasing power and investment returns. Central banks’ responses to inflation, particularly interest rate adjustments, will significantly influence bond yields, equity valuations, and overall market liquidity. A hawkish stance could lead to tighter credit conditions, potentially slowing economic growth, while a dovish pivot might reignite inflationary pressures.

Geopolitical events continue to cast a long shadow over global markets. Regional conflicts, trade disputes, and international political shifts can introduce sudden and unpredictable volatility. Such events often trigger flight-to-safety behaviors, impacting currency valuations and commodity prices. For instance, disruptions in energy supplies can lead to spikes in oil and gas prices, directly affecting consumer spending and corporate profits. Similarly, political instability in key manufacturing hubs can disrupt global supply chains, leading to shortages and increased costs.

Technological advancements, while generally positive for long-term growth, can also create short-term market dislocations. Rapid innovation in areas like artificial intelligence, quantum computing, and biotechnology can lead to significant shifts in industry leadership, rendering some traditional businesses obsolete while propelling others to unprecedented heights. Investors need to be mindful of these disruptive forces and their potential impact on established companies within their portfolios.

Furthermore, domestic economic factors, such as employment rates, consumer confidence, and corporate earnings, will provide crucial insights. A robust job market and strong consumer spending can underpin economic stability, while any signs of weakening could signal a slowdown. Corporate earnings reports will reveal the health of individual companies and sectors, influencing investor sentiment and stock performance. Analyzing these factors collectively helps in forming a more holistic view of the market environment you’ll be navigating.

The interplay of these factors creates a dynamic and often unpredictable market environment. Therefore, a static investment approach is unlikely to suffice. Instead, a flexible and adaptive strategy is essential to both mitigate risks and capitalize on emerging opportunities. This proactive mindset is fundamental to knowing how to protect retirement portfolio effectively.

Re-evaluating Your Risk Tolerance and Investment Horizon

Before implementing any new strategies, a critical self-assessment of your personal financial situation is paramount. Your risk tolerance, which is your ability and willingness to take on investment risk, should be revisited, especially in light of impending market volatility. Are you comfortable with significant fluctuations, or do you prefer a more conservative approach that prioritizes capital preservation? For retirees, the answer often leans towards preservation, as there is less time to recover from substantial losses.

Your investment horizon also plays a crucial role. If you are in the early stages of retirement, your horizon might still be quite long, allowing for a degree of growth-oriented investments. However, if you are approaching or are in the later stages of retirement, your horizon is considerably shorter, necessitating a greater emphasis on income generation and capital protection. A shorter horizon means less time for the market to rebound from a downturn, making significant losses much more impactful.

Consider your immediate and future income needs. Do you rely heavily on your portfolio for living expenses, or do you have other stable income sources like pensions or annuities? The more dependent you are on your portfolio for income, the greater the need for stability and predictability. This assessment helps in determining the appropriate balance between growth assets and income-generating assets within your portfolio.

It’s also wise to assess your emergency fund. Having readily accessible cash or highly liquid assets separate from your investment portfolio can provide a crucial buffer during volatile periods, preventing you from having to sell investments at a loss to cover unexpected expenses. A robust emergency fund reduces the pressure on your investment portfolio and allows it to weather market storms more effectively.

Engaging in a candid conversation with a trusted financial advisor can provide invaluable insights during this re-evaluation process. They can help you objectively assess your risk profile, understand the implications of different investment choices, and align your portfolio with your specific retirement goals and current life stage. This foundational step is indispensable for anyone looking to truly protect retirement portfolio assets.

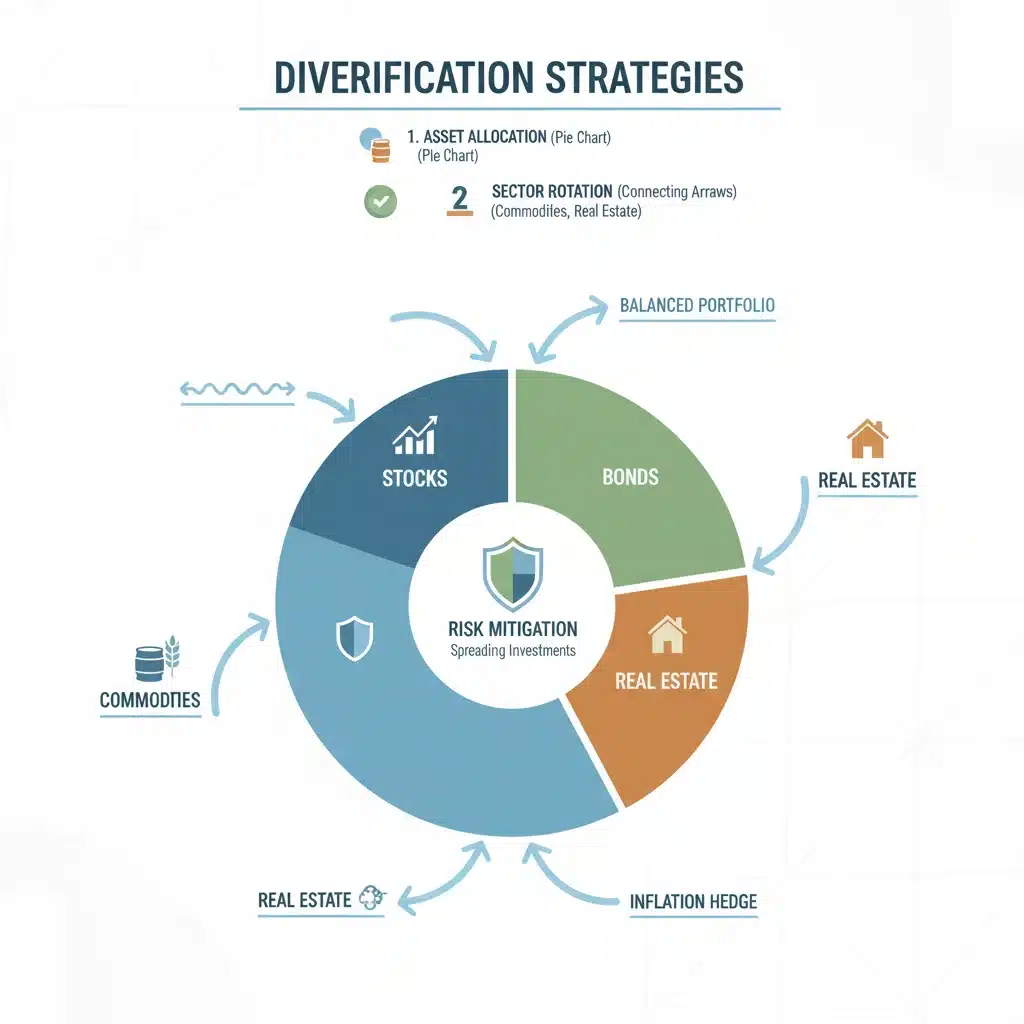

Diversification: Your First Line of Defense

Diversification remains the cornerstone of any robust investment strategy, and its importance is amplified during periods of market volatility. The adage, ‘don’t put all your eggs in one basket,’ holds more truth than ever. Diversification involves spreading your investments across various asset classes, industries, geographies, and investment styles to reduce overall risk. If one segment of the market performs poorly, others may perform well, helping to smooth out returns and mitigate losses.

Asset Class Diversification

This is the most fundamental form of diversification. It involves allocating your investments across different asset classes such as:

- Equities (Stocks): While offering potential for capital appreciation, they also come with higher volatility. Within equities, diversify across sectors (e.g., technology, healthcare, consumer staples) and market capitalizations (large-cap, mid-cap, small-cap).

- Fixed Income (Bonds): Generally less volatile than stocks, bonds can provide a steady stream of income and act as a hedge during equity downturns. Diversify by bond type (government, corporate, municipal), credit quality, and maturity dates.

- Real Estate: Can offer long-term appreciation and income. This can be direct ownership, Real Estate Investment Trusts (REITs), or real estate funds.

- Commodities: Such as gold, silver, oil, or agricultural products, can act as inflation hedges and provide diversification benefits, especially during periods of economic uncertainty.

- Cash and Cash Equivalents: Essential for liquidity and as a safe haven during extreme volatility.

Geographic Diversification

Investing solely in your home country exposes you to concentrated economic and political risks. Spreading investments across different countries and regions can reduce this concentration. Global markets often move independently, so a downturn in one region might be offset by growth in another. This can include developed markets, emerging markets, and frontier markets, each with its own risk-reward profile.

Sector and Industry Diversification

Within equities, avoid overconcentration in a single sector. Economic cycles and technological shifts can disproportionately affect certain industries. For example, during a recession, consumer discretionary stocks might suffer, while healthcare or utility stocks might remain more stable. A well-diversified portfolio will have exposure to various sectors to minimize the impact of any single industry’s poor performance.

Investment Style Diversification

This refers to investing in different types of funds or stocks based on their investment philosophy. Examples include growth investing (focusing on companies with high growth potential), value investing (focusing on undervalued companies), and income investing (focusing on dividend-paying stocks or high-yield bonds). Combining these styles can provide a more balanced risk-return profile.

The goal of diversification is not to eliminate risk entirely, but to manage it. No investment is without risk, but by spreading your investments wisely, you can significantly reduce the impact of any single negative event on your overall portfolio. Regularly review and rebalance your diversified portfolio to ensure it remains aligned with your risk tolerance and financial objectives, particularly as market conditions evolve. This is a continuous effort to effectively protect retirement portfolio assets.

Strategic Asset Allocation and Rebalancing

Once you’ve established your desired level of diversification, the next crucial step is strategic asset allocation. This involves determining the optimal mix of asset classes in your portfolio based on your age, risk tolerance, and financial goals. For retirees, this often means a shift towards a more conservative allocation, emphasizing capital preservation and income generation over aggressive growth.

A common guideline for asset allocation for retirees is the ‘rule of 100 minus your age’ for equity exposure, though this is a simplistic starting point and should be adjusted based on individual circumstances. For example, a 70-year-old might consider having 30% in equities and 70% in fixed income and other less volatile assets. However, a healthy 70-year-old with a long life expectancy and stable income might comfortably hold a higher percentage in equities.

The Role of Fixed Income

In a volatile market, fixed-income investments, particularly high-quality bonds, can act as a ballast, providing stability and predictable income. While their returns might be lower than equities during bull markets, their ability to preserve capital during downturns is invaluable for retirees. Consider a laddered bond portfolio, where bonds mature at different intervals, providing regular cash flow and allowing you to reinvest at prevailing interest rates.

Cash and Short-Term Investments

Maintaining a healthy allocation to cash and short-term investments is vital. This provides liquidity for immediate spending needs, unexpected expenses, and allows you to avoid selling long-term investments at a loss during market dips. It also positions you to take advantage of buying opportunities when asset prices are low.

The Art of Rebalancing

Market fluctuations will inevitably cause your portfolio’s asset allocation to drift from its target. Rebalancing is the process of adjusting your portfolio back to your original target allocation. For instance, if equities have performed well, they might now represent a larger percentage of your portfolio than intended. Rebalancing would involve selling some of those appreciated equities and reinvesting the proceeds into underperforming assets (like bonds) to restore your desired balance.

Rebalancing serves several critical purposes:

- Risk Management: It prevents your portfolio from becoming overly concentrated in assets that have performed exceptionally well, which might also carry higher risk.

- Discipline: It enforces a disciplined approach to investing, forcing you to ‘buy low and sell high’ (or at least sell high and buy low), rather than chasing hot trends.

- Alignment with Goals: It ensures your portfolio continues to align with your risk tolerance and long-term financial objectives, which is especially important as you age.

The frequency of rebalancing can vary. Some investors prefer to rebalance annually or semi-annually, while others might do so when an asset class deviates by a certain percentage from its target allocation (e.g., 5% or 10%). The key is to have a consistent strategy. Strategic asset allocation and diligent rebalancing are proactive measures that significantly help to protect retirement portfolio assets from market swings.

Exploring Alternative Investments for Portfolio Protection

Beyond traditional stocks and bonds, alternative investments can offer additional diversification and potential for uncorrelated returns, which can be invaluable during periods of market volatility. These investments often behave differently from conventional assets, providing a buffer when traditional markets are struggling. However, they also come with their own set of risks and complexities, requiring careful consideration.

Gold and Precious Metals

Historically, gold has been considered a safe-haven asset, often performing well during times of economic uncertainty, geopolitical instability, and high inflation. It tends to have a low correlation with equities, meaning its price movements are often independent of the stock market. Investors can gain exposure to gold through physical bullion, gold ETFs, or mining stocks.

Real Estate (Beyond Traditional Stocks)

While REITs offer liquidity and diversification, direct real estate investments (e.g., rental properties, land) can provide tangible assets with potential for rental income and capital appreciation. These investments are less liquid than publicly traded securities but can offer a hedge against inflation and market downturns, provided they are well-managed and financed prudently.

Annuities

Annuities are insurance contracts designed to provide a steady stream of income during retirement. Fixed annuities offer guaranteed returns and principal protection, while indexed annuities offer market-linked returns with some downside protection. Variable annuities, while offering higher growth potential, also carry more market risk. For retirees seeking guaranteed income and capital protection, certain types of annuities can be a valuable addition to protect retirement portfolio income streams.

Private Equity and Venture Capital

These investments involve owning stakes in private companies. They are typically illiquid and require a long-term commitment, but they can offer significant growth potential and diversification from public markets. Access to these investments is often restricted to accredited investors through specialized funds.

Managed Futures

Managed futures strategies involve investing in a wide range of futures contracts across various asset classes (commodities, currencies, interest rates, equities). These strategies are often managed by professional commodity trading advisors (CTAs) who aim to profit from both rising and falling markets. They can provide significant diversification benefits due to their low correlation with traditional assets.

Considerations for Alternative Investments

- Liquidity: Many alternative investments are illiquid, meaning they cannot be easily converted to cash without significant loss. This is a critical consideration for retirees who may need access to funds.

- Complexity: They often involve complex structures and require a deeper understanding than traditional investments.

- Fees: Alternative investments typically come with higher fees compared to mutual funds or ETFs.

- Due Diligence: Thorough research and professional advice are essential before investing in alternatives.

While alternative investments can enhance portfolio resilience, they are not suitable for all investors. Their inclusion should be carefully weighed against your overall financial plan, risk tolerance, and liquidity needs. A small allocation to carefully selected alternatives can be a powerful tool to protect retirement portfolio from the vagaries of traditional markets.

Tax-Efficient Withdrawal Strategies and Income Planning

Protecting your retirement portfolio isn’t just about investment choices; it’s also about how you manage your income and withdrawals. Tax efficiency can significantly impact the longevity of your savings, especially during volatile periods. A well-thought-out withdrawal strategy can minimize your tax burden and preserve capital.

Sequence of Withdrawals

The order in which you draw from different retirement accounts can have a profound impact. A common strategy, especially during market downturns, is to prioritize withdrawals from taxable accounts first, then tax-deferred accounts (like traditional IRAs and 401(k)s), and finally tax-free accounts (like Roth IRAs and 401(k)s). This approach allows your tax-advantaged accounts, particularly Roth accounts, to continue growing tax-free, potentially for longer periods, and recover from market dips.

Required Minimum Distributions (RMDs)

Remember that RMDs from traditional IRAs and 401(k)s typically begin at age 73 (or 75 depending on your birth year), and these withdrawals are taxable. Planning for RMDs is crucial, as they can significantly impact your taxable income and potentially push you into a higher tax bracket. Strategic Roth conversions in years with lower income or market downturns can help mitigate future RMD burdens.

Consider Tax-Loss Harvesting

During market downturns, you might have investments in taxable accounts that are trading at a loss. Tax-loss harvesting involves selling these investments to realize the loss, which can then be used to offset capital gains and potentially up to $3,000 of ordinary income per year. While you can reinvest the proceeds into a similar but not identical investment (to avoid the wash-sale rule), this strategy can reduce your current tax liability and effectively protect retirement portfolio value by offsetting other gains.

Guaranteed Income Sources

Incorporating guaranteed income sources, such as annuities, pensions, or Social Security, can reduce your reliance on your investment portfolio for daily living expenses. This stability allows your portfolio to weather market storms without the pressure of forced sales. Maximizing Social Security benefits by delaying claims until age 70, if feasible, can also provide a substantial and inflation-adjusted income stream.

Budgeting and Spending Control

In times of market uncertainty, revisiting your budget and controlling discretionary spending can be a powerful protective measure. Reducing withdrawals from your portfolio during a downturn allows more time for your investments to recover, preserving capital for the long term. This proactive management of your outflow is as important as managing your inflow and investment growth.

A holistic approach that integrates investment management with tax planning and income strategy is vital. Consult with a tax advisor and financial planner to develop a withdrawal strategy tailored to your specific circumstances and designed to maximize the longevity of your retirement savings while minimizing your tax burden. This integrated approach is fundamental to truly protect retirement portfolio assets.

The Role of Professional Financial Advice

While this guide provides a wealth of information, navigating the complexities of Q1 2026 market volatility and implementing sophisticated strategies to protect retirement portfolio assets can be challenging. This is where the expertise of a qualified financial advisor becomes invaluable. A professional advisor offers more than just investment recommendations; they provide a comprehensive, personalized approach to your financial well-being.

Personalized Planning

An advisor can help you create a personalized financial plan that takes into account your unique circumstances, including your current assets, liabilities, income sources, expenses, health status, and specific retirement goals. They can objectively assess your true risk tolerance and capacity for risk, which might differ from your perceived comfort level.

Objective Perspective

During periods of market stress, emotions often run high. Fear can lead to impulsive decisions, such as selling low, while greed can lead to chasing unsustainable gains. A financial advisor provides an objective, disciplined perspective, helping you stick to your long-term plan and avoid emotionally driven mistakes that can significantly harm your portfolio. They act as a behavioral coach, guiding you through the ups and downs of the market.

Expertise in Complex Strategies

Implementing strategies like sophisticated asset allocation, tax-loss harvesting, Roth conversions, and integrating alternative investments requires specialized knowledge. An advisor is well-versed in these areas and can help you execute them effectively, ensuring compliance with regulations and optimizing outcomes. They stay abreast of the latest market trends, economic forecasts, and regulatory changes that could impact your portfolio.

Ongoing Monitoring and Adjustment

Markets are dynamic, and your personal circumstances can change. A good financial advisor provides ongoing monitoring of your portfolio’s performance and makes necessary adjustments. They will schedule regular reviews to ensure your plan remains aligned with your goals and to adapt to any shifts in market conditions or your personal life, such as health changes or unexpected expenses.

Estate Planning Integration

Beyond investment management, a comprehensive financial advisor can help integrate your retirement plan with your broader estate plan, ensuring that your assets are distributed according to your wishes and minimizing potential estate taxes for your beneficiaries. This holistic approach ensures that all aspects of your financial life are working in harmony.

Choosing the right advisor is crucial. Look for a Certified Financial Planner (CFP) or a fee-only fiduciary advisor who is legally bound to act in your best interest. Interview several candidates to find someone whose philosophy aligns with yours and with whom you feel comfortable discussing your most personal financial details. Investing in professional financial advice can be one of the most effective ways to protect retirement portfolio assets and secure a confident retirement.

Conclusion: Proactive Measures for a Secure Retirement

The prospect of Q1 2026 market volatility, while potentially unsettling, does not have to be a source of overwhelming anxiety for retirees. By adopting a proactive, informed, and disciplined approach, you can significantly enhance your ability to protect retirement portfolio assets and maintain your financial security. The strategies outlined in this guide – understanding market dynamics, re-evaluating risk, embracing diversification, implementing strategic asset allocation and rebalancing, exploring suitable alternative investments, and optimizing tax-efficient withdrawal strategies – form a powerful framework for resilience.

Remember that timing the market is notoriously difficult, even for seasoned professionals. Instead of reacting to every market swing, focus on building a robust, diversified portfolio that can withstand various economic conditions. Your retirement is a culmination of years of hard work and sacrifice; it deserves careful and continuous attention.

Regularly review your financial plan, stay informed about global economic trends, and, perhaps most importantly, seek professional guidance when needed. A trusted financial advisor can be an invaluable partner in navigating complex market environments, offering expert insights, objective advice, and the peace of mind that comes from knowing your financial future is in capable hands.

By taking these practical, time-sensitive steps now, you are not just reacting to potential threats; you are actively building a stronger, more resilient retirement portfolio. This proactive stance ensures that you can face Q1 2026 and subsequent years with confidence, knowing that you have taken all necessary measures to safeguard your financial well-being and enjoy the retirement you’ve worked so hard for.